by Gita Gopinath*

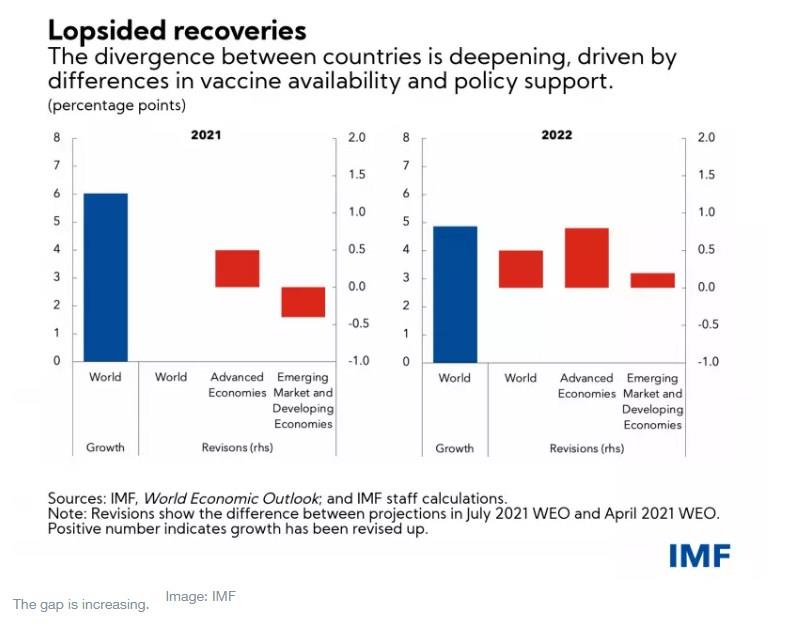

The global economic recovery continues, but with a widening gap between advanced economies and many emerging market and developing economies. Our latest global growth forecast of 6 percent for 2021 is unchanged from the previous outlook, but the composition has changed.

Growth prospects for advanced economies this year have improved by 0.5 percentage point, but this is offset exactly by a downward revision for emerging market and developing economies driven by a significant downgrade for emerging Asia. For 2022, we project global growth of 4.9 percent, up from our previous forecast of 4.4 percent. But again, underlying this is a sizeable upgrade for advanced economies, and a more modest one for emerging market and developing economies.

We estimate the pandemic has reduced per capita incomes in advanced economies by 2.8 percent a year, relative to pre-pandemic trends over 2020-2022, compared with an annual per capita loss of 6.3 percent a year for emerging market and developing economies (excluding China).

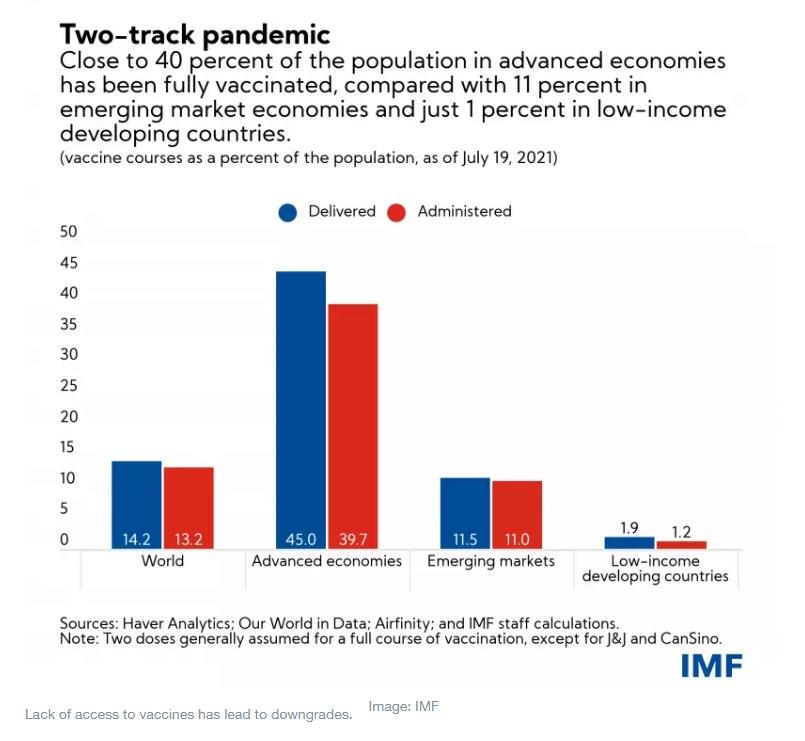

These revisions reflect to an important extent differences in pandemic developments as the delta variant takes over. Close to 40 percent of the population in advanced economies has been fully vaccinated, compared with 11 percent in emerging market economies, and a tiny fraction in low-income developing countries. Faster-than-expected vaccination rates and return to normalcy have led to upgrades, while lack of access to vaccines and renewed waves of COVID-19 cases in some countries, notably India, have led to downgrades.

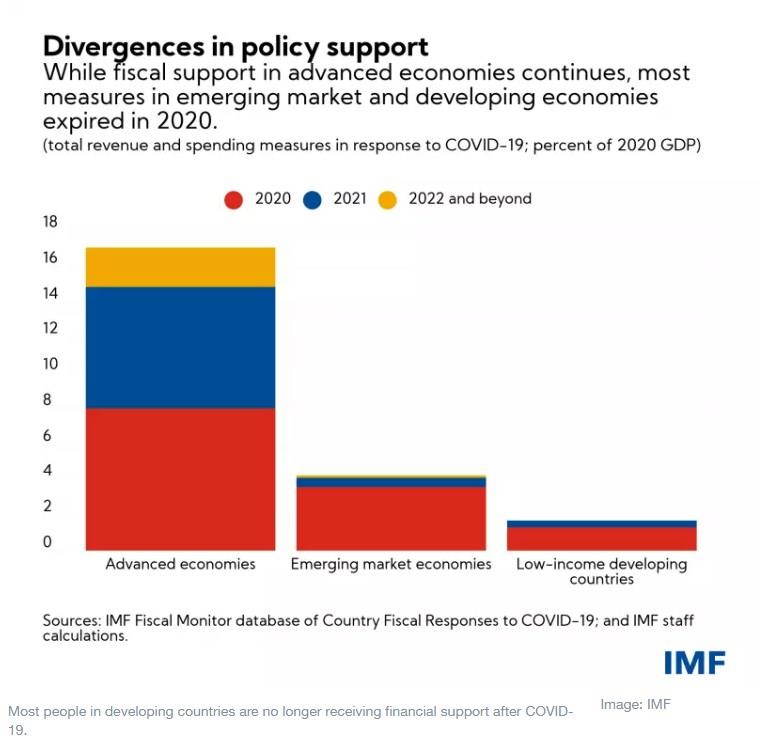

Divergences in policy support are a second source of the deepening divide. We are seeing continued sizable fiscal support in advanced economies with $4.6 trillion of announced pandemic related measures available in 2021 and beyond. The upward global growth revision for 2022 largely reflects anticipated additional fiscal support in the United States and from the Next Generation European Union funds.

On the other hand, in emerging market and developing economies most measures expired in 2020 and they are looking to rebuild fiscal buffers. Some emerging markets like Brazil, Hungary, Mexico, Russia, and Turkey, have also begun raising monetary policy rates to head off upward price pressures. Commodity exporters have benefited from higher-than-anticipated commodity prices.

Inflation concerns

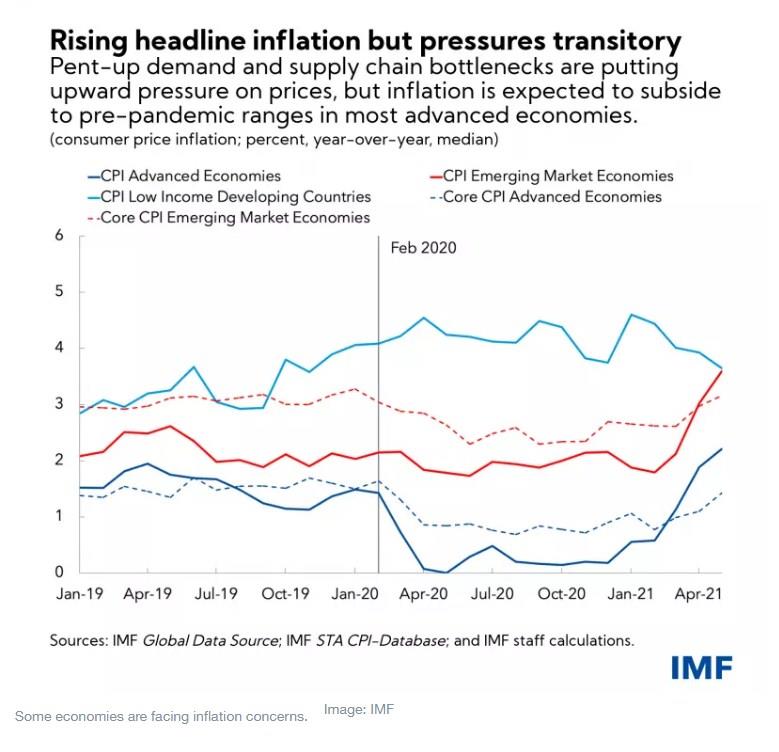

Aftershocks from the upheaval of last year pose unique policy challenges. Pent-up demand and supply chain bottlenecks are putting upward pressure on prices. Nonetheless, in most advanced economies inflation is expected to subside to pre-pandemic ranges in 2022 for the following reasons:

First, a significant fraction of the abnormally high inflation readings is transitory, resulting from pandemic affected sectors such as travel and hospitality, and from comparison with last year’s abnormally low readings such as for commodity prices.

Second, overall employment rates remain well below pre-pandemic levels in most countries and while there has been rapid wage growth in some sectors, overall wage growth remains within normal ranges. As health metrics improve and exceptional income support measures expire, hiring difficulties in certain sectors are expected to abate and ease wage pressures.

Third, long-term inflation expectations (as measured by surveys and market-based measures) remain well-anchored, and factors such as automation that have lowered the sensitivity of prices to changes in labor market slack likely have intensified through the pandemic.

This assessment is, however, subject to significant uncertainty given the uncharted nature of this recovery. More persistent supply disruptions and sharply rising housing prices are some of the factors that could lead to persistently high inflation. Further, inflation is expected to remain elevated into 2022 in some emerging market and developing economies, related in part to continued food price pressures and currency depreciations—creating yet another divide.

While more widespread vaccine access could improve the outlook, risks on balance are tilted to the downside. The emergence of highly infectious virus variants could derail the recovery and wipe out $4.5 trillion cumulatively from global GDP by 2025. Financial conditions could also tighten abruptly amid stretched asset valuations, if there is a sudden reassessment of the monetary policy outlook, especially in the United States. It is also possible that stimulus spending in the United States could prove weaker than expected. A worsening pandemic and tightening financial conditions would inflict a double hit on emerging market and developing economies and severely set back their recoveries.

Policies to arrest divergences and improve prospects

Multilateral action is needed to ensure rapid, worldwide access to vaccines, diagnostics, and therapeutics. This would save countless lives, prevent new variants from emerging, and add trillions of dollars to global economic growth. IMF staff’s recent proposal to end the pandemic, endorsed by the World Health Organization, World Bank, and World Trade Organization, sets a goal of vaccinating at least 40 percent of the population in every country by the end of 2021 and at least 60 percent by mid-2022, alongside ensuring adequate diagnostics and therapeutics at a price of $50 billion.

To achieve these targets, at least 1 billion vaccine doses should be shared in 2021 by countries with surplus vaccines, and vaccine manufacturers should prioritize deliveries to low- and lower-middle income countries. It is important to remove trade restrictions on vaccine inputs and finished vaccines and make additional investment in regional vaccine capacity to ensure sufficient production. It is essential to also make available upfront grant financing of around $25 billion for diagnostics, therapeutics, and vaccine preparedness for low-income developing countries.

A related priority is to ensure that financially constrained economies maintain access to international liquidity. Major central banks should clearly communicate their outlook for monetary policy and ensure that inflation fears do not trigger rapid tightening of financial conditions. A general allocation of Special Drawing Rights (SDR) equivalent to $650 billion ($250 billion to emerging market and developing economies), as proposed by the IMF, should be completed quickly so as to provide liquidity buffers for countries and help them address their essential spending needs. The impact can be further magnified if rich nations voluntarily channel their SDRs to emerging market and developing economies. Finally, greater action is needed to ensure that the G20 Common Framework successfully delivers on debt restructuring for countries where debt is already unsustainable.

The other major shared challenge is to reduce carbon emissions and slow the rise in global temperatures to avoid catastrophic health and economic outcomes. A multipronged strategy with carbon pricing as its centerpiece will be needed. Revenue from carbon pricing mechanisms should be used to fund compensatory transfers to those hurt by the energy transition. In parallel, a green infrastructure push and subsidies for research into green technologies are needed to hasten the move to lower carbon dependence. So far, only 18 percent of recovery spending has been on low-carbon activities.

National level policies needed to reinforce multilateral efforts for securing the recovery

Policy efforts at the national level should continue to be tailored to the stage of the pandemic:

-First, to escape the acute crisis by prioritizing health spending, including for vaccinations, and targeted support for affected households and firms;

-Next, to secure the recovery with more emphasis on broader fiscal and monetary support, depending on available space, including remedial measures to reverse the loss in education, and supporting the reallocation of labor and capital to growing sectors through targeted hiring subsidies and efficient bankruptcy resolution mechanisms; and

-Finally, to invest in the future, by advancing long-term goals of boosting productive capacity, accelerating the transition to lower carbon dependence, harnessing the benefits of digitalization, and ensuring the gains are equitably shared.

Fiscal actions should be nested within a credible medium-term fiscal framework to ensure debt remains sustainable. For many countries this will involve improving tax capacity, increasing tax progressivity, and eliminating wasteful expenditures. Low-income developing countries will also need strong international support.

Central banks should avoid prematurely tightening policies when faced with transitory inflation pressures but should be prepared to move quickly if inflation expectations show signs of de-anchoring. Emerging markets should also prepare for possibly tighter external financial conditions by lengthening debt maturities where possible and limiting the buildup of unhedged foreign currency debt.

The recovery is not assured until the pandemic is beaten back globally. Concerted, well-directed policy actions at the multilateral and national levels can make the difference between a future where all economies experience durable recoveries or one where divergences intensify, the poor get poorer, and social unrest and geopolitical tensions grow.

*Chief Economist, International Monetary Fund (IMF)

**first published in: www.weforum.org

By: N. Peter Kramer

By: N. Peter Kramer