by Gulcin Ozkan*

National economies are beginning to return to their pre-pandemic levels. But like the uneven impact of the pandemic itself, the pace of economic recovery is massively divergent across countries.

In 2020, the global economy contracted by 4.3%, with some countries doing considerably worse than others. For example, the UK economy suffered its worst recession in 300 years, shrinking by nearly 10%. The resulting impact on jobs was also unprecedented, and ten times worse than during the 2009 global financial crisis, with 114 million jobs lost globally in 2020.

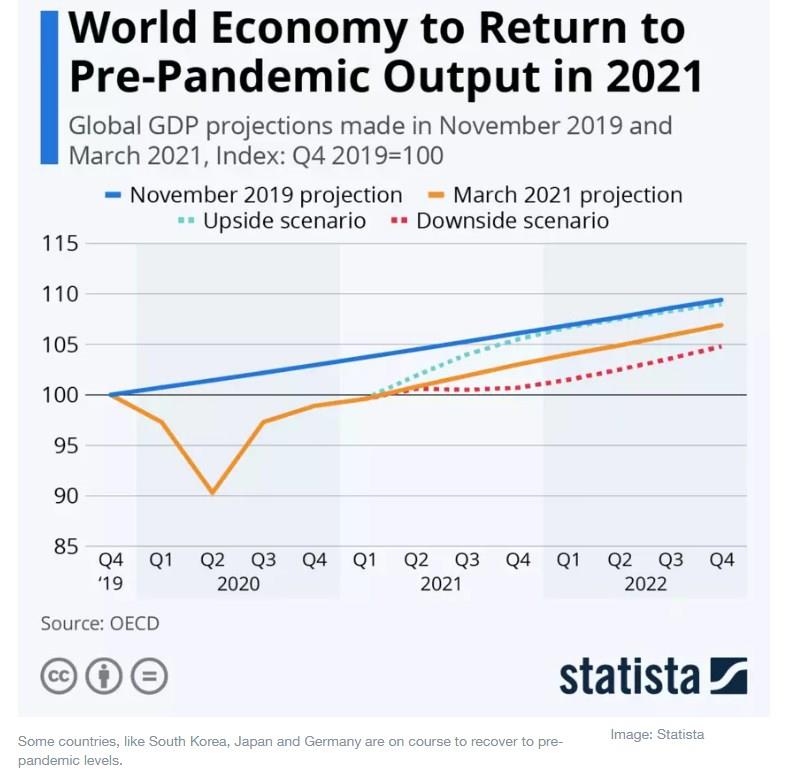

More than a year on from the start of the pandemic, global prospects appear to be improving, according to recent reports by the OECD and the World Economic Forum. The data shows that some countries – such as the US, South Korea, Japan and Germany – are on course to recover to pre-pandemic levels of GDP per capita by the end of 2021.

But others, such as Spain and Iceland, both of whom suffered a huge blow from the collapse in tourism revenues, are expected to operate below pre-pandemic levels until at least mid-2023. Worse still, countries such as South Africa and Argentina are forecast to remain below their 2019 levels until the end of 2024, or well into 2025.

Uneven recovery

Two main factors underpin the speed of a country’s economic recovery from the pandemic: the strength of its COVID-19 policy response, and the success of its vaccination programme.

Unsurprisingly, the UK and the US, with the highest projected growth rates among advanced economies – 7.2% and 6.9%, respectively – also top the league tables for size of pandemic response policy packages and share of the population successfully vaccinated.

Leaders across the globe deployed a range of economic policy responses in the fight against the pandemic. Public spending measures included transfers to (low-income) households, grants and tax holidays to businesses, and additional funding for healthcare systems. Some supplemented conventional interest rate cuts with unconventional measures such as liquidity injections and asset purchases. Many governments also used financial measures including foreign exchange interventions.

Importantly, policy action varied significantly across countries in type, size and scope. The pandemic hit emerging markets harder than advanced economies, unlike in the aftermath of the 2008 global financial crisis. Many poorer countries have found it harder to contain and mitigate the virus because of their limited healthcare capacity, and with less ability to expand public spending, suffered greater losses from the pandemic.

The divergence in recovery can also be linked to the varying success of national vaccination programs – as the OECD put it, “more jabs, more jobs”. For example, while Israel has vaccinated about 60% of its population, in many other countries, fewer than one in ten have received any vaccinations. Israel’s economy is expected return to pre-pandemic levels by early 2022.

What is worse, many poor countries may see almost no vaccinations until at least the end of 2021. This – and the significant ongoing variation in both infection and death rates – suggests that the pattern of recovery from the public health crisis will also be uneven.

Global consequences

This multispeed recovery from the pandemic and the ensuing economic crisis will have repercussions, not just for the countries with slower recoveries but also for the global economy. On the health front, no country will be fully safe from the virus until all are safe. Local vaccination successes will not be sufficient to protect individual countries from potential further outbreaks, especially in cases of new variants.

But divergence in the speed and scale of economic recovery also entails substantial risk to individual countries as well as their trading partners. The COVID-19 economic crisis has exposed the fragility of existing international trade structures, where countries are highly dependent on one another. These interdependencies arise from the global value chains – production broken into multiple stages and completed in different countries – accounting for 70% of current global trade..

One example of the global economy’s reliance on certain countries is the shortage of semiconductors, the microchips used in the production of every electronic device from mobile phones to home appliances. Lockdowns in the early days of the pandemic affected the major producers, including China, creating a significant shortage of semiconductors. This led to production bottlenecks of electronic goods in many other countries, forcing a serious rethink of the costs versus benefits of global supply chains.

The pandemic and related economic crisis have also had different effects within national boundaries. In many countries, inequality has widened significantly in multiple ways. Less well-off households have lost out much more than those at the top of the income distribution, and there has also been a much more substantial contraction in contact-based service industries than in other sectors.

A significant rebalancing will be an important step in a successful transition to a post-COVID world. In terms of international policy coordination, the immediate challenge is how rich and poor countries can work together to increase the vaccine coverage rates in as many countries as possible. The COVAX programme – an international effort led by the WHO to provide vaccines to poor nations – and the problems it currently faces show that while such international coordination is possible, it is fraught with difficulty.

On economic recovery, too, national gains are unlikely to be long-lasting if a significant part of the world remains behind.

*Professor of Finance, King’s College London

**first published in: www.weforum.org

By: N. Peter Kramer

By: N. Peter Kramer