by Gayle Markovitz and Linda Lacina*

Sustainable finance is the practice of taking environmental, social, and governance (ESG) considerations into account when making investment decisions. Today investment funds that use ESG have more than $50 trillion in capital and are growing fast.

The trend is contentious, with detractors warning that funds must offer tangible solutions, without distracting governments, central banks, policy-makers, investors and business leaders from the scale of the global climate challenge, which requires ambitious systemic change.

And there are calls for transparent and harmonized sustainability metrics that involve consumers and measure the impact of companies on the communities in which they operate.

There is much effort going into the pricing of sustainability initiatives, such as net-zero targets and protecting biodiversity. But as Mckinsey research highlights “while a number of analytic perspectives explain how greenhouse-gas emissions would need to evolve to achieve a 1.5-degree pathway, few paint a clear and comprehensive picture of the actions global business could take to get there.”

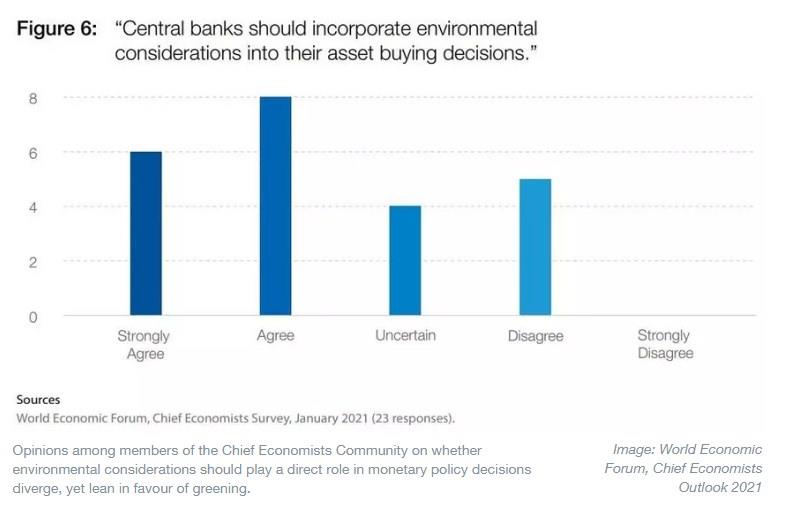

Opinions among chief economists also diverge on whether environmental considerations should play a direct role in monetary policy decisions.

Manuela Fulga, Platform Curator, Banking and Capital Markets, World Economic Forum emphasizes the potential of tech to realize emissions-busting ambitions, “The good news is that both public and private stakeholders from industries, finance and governments have announced ambitious pledges to reduce carbon emissions: net-zero commitments today cover ~68% of global GDP”, yet she warns, “translating commitments to action is no simple undertaking.”

The challenge is similarly daunting when it comes to nature. The recent State of Finance for Nature report found that investments in nature will have to triple by 2030 and increase four-fold by 2050 from the current investments of $133 billion. Forest-based solutions alone, including the management, conservation and restoration of forests, will require $203 billion annually, which is just over $25 per year for every citizen in 2021.

How then can we ensure that sustainable solutions get the funding, support and financial backing they need?

We asked 4 experts to identify what must change to ensure such solutions can be deployed to their fullest potential. They reveal their strategies to promote investments and approaches that are making things like the energy transition and other key shifts possible.

‘Early-stage capital… multiple funding partners’

Jacob Duer, President and CEO, Alliance to End Plastic Waste

Driving a circular economy for plastics requires significant investments to build the necessary waste management infrastructure and innovation ecosystems. In the absence of coordinated action among governments, funding organizations and practitioners, the financial burden and risk for any single investor or group of investors is too high to drive the needed change across the entire plastic economy.

The Indonesia National Plastic Action Partnership (NPAP) established that, in Indonesia alone, an estimated US$17 billion in capital investment and a further US$1 billion of annual operational expenditure are required between today and 2040 if levels of plastic waste collection and recycling are to meet the ambitious goals set by the Indonesian Government. The Alliance to End Plastic Waste, a member of the NPAP Indonesia Financing Task Force, provides early-stage capital and takes on early development risks.

For example, a new multi-million Alliance-led programme in Indonesia aims to develop new integrated waste management systems on the island of Java. The first phase aims to serve 2.5 million people and divert up to 40,000 tons of plastic waste from the environment every year.

The project in Indonesia builds on the early impact seen from previous experience with innovative financing models. In Ghana, the Alliance has supported the ASASE Foundation to empower women entrepreneurs working to eliminate plastic litter through recycling. The project has scaled up operations of its CASH IT! recycling facility in Accra to 2,000 metric tons in 2021, up from 35 metric tons in 2018. Based on this result, the initiative has now secured additional funding from the European Commission to scale up the model.

These are examples of multiple financing partners working together and co-investing, with each providing unique capabilities and reducing overall risk. The Global Plastic Action Partnership (GPAP) and its growing network of country-level multistakeholder platforms is a key enabler for such powerful collaborations. Only through partnership in action and in financing can we put an end to plastic pollution.

‘Sovereign wealth funds must go green’

Gunther Thallinger, Member of the Board of Management of Allianz SE and Chair of the UN-convened Net-Zero Asset Owner Alliance

Net-zero initiatives are established in the banking, investment management and institutional investor industries. However, the world’s 90-plus sovereign wealth funds (SWFs), which oversee more than $9.7 trillion in assets, are lagging.

The pressing issue is that greenhouse gases are measured at the country level. However, this understates the climate impact countries have via SWFs with extensive foreign assets.

For example, the largest SWF, the Government Pension Fund of Norway holds assets of $1.3 trillion – three times Norway’s economy. The carbon footprint is 107.6m tonnes, twice the country’s annual emissions. Despite this, the fund does not have specific emissions reduction targets or adopted a climate-adjusted equity benchmark.

Norway is not alone. SWFs are often owned by governments with ambitious climate objectives. However, three-quarters have less than 10% of holdings in climate-related strategies, while only 14% had made divestment decisions related to climate or environmental targets. Further, only 12% have an explicit climate-change policy.

It is disingenuous to pretend emissions linked to SWFs are separate climate change. Governments should be consistent in their climate ambitions and ensure SWF investments match national goals. Most SWFs were established as savings vehicles for future generations. Their investments should contribute to the conservation of the climate that those generations will live in.

‘For a low-carbon future, investors should focus on additionality’

James Gifford, Head of Sustainable & Impact Advisory and Thought Leadership, Credit Suisse

Investors play a key role in getting to net zero. But not all sustainable investments are created equal when it comes to impact. To create real impact, investors need to demonstrate additionality: that is, is there less carbon emitted because of the investment?

There are two key mechanisms of additionality within investment, and investors need to be laser focused on these:

-Seed and growth capital into illiquid investments, specifically, venture capital funds backing early-stage companies focused on climate innovation. If the whole world is to transition from fossil fuels, cleaner alternatives simply need to be cheaper, and this will require funding of rapid innovation.

-Active ownership in liquid public markets. Simply buying or selling stock in liquid markets from other investors makes little measurable impact. But shareholder engagement has a 30-year track record of effectiveness in pushing companies to improve. Coalitions such as Climate Action 100+ are aggregating capital representing close to half of global capital markets to collectively push companies to reduce emissions.

Sustainable investing is no silver bullet. However, it can be an important part of the solution, especially if the focus is on strategies that are most impactful.

‘Capital can be transformative’

Greg Guyett, Co-CEO of Global Banking & Markets, HSBC

The net zero transition will require investment – between $1-2 trillion each and every year until 2050. That number looks daunting, but it is achievable if policy-makers, the financial sector and businesses quickly shift gear. It’s also critical to enable the continued development of many of the world’s economies and improve the lives of millions of people.

A successful global transition requires deep collaboration with business sectors which today are the heaviest emitters, such as transportation, power generation and steel production. These industries will see fundamental shifts over the course of the next decades and require capital to finance the development and deployment of new technologies to reduce their emissions.

Capital can be transformative where it is linked to commitments that align to the goals of the Paris Agreement. For instance, where the interest rate on a debt instrument is tied to emissions reduction targets. HSBC recently worked with global petrol company Repsol to embed its commitment to reduce its carbon emissions in its debt financing. The transition won’t happen overnight, but sustainable finance can create accountability to ensure we are progressing at pace towards our collective net zero ambitions.

Policy-makers should work in tandem with the financial sector to incentivize the transformation of business models towards net zero. The capabilities and infrastructure of large companies in high-emission sectors must not be discounted. Given the right conditions, they can attract capital to deliver emissions reduction at scale. And scale is critical to addressing the climate crisis.

*Partnerships Editor, World Economic Forum and Digital Editor, World Economic Forum

**first published in: www.weforum.org

By: N. Peter Kramer

By: N. Peter Kramer