by Ami Daniel and Lord John Browne*

Of the 14 trillion dollars spent each year on transportation, over 90 percent goes on journeys by sea. Ocean freight vessels are large and getting bigger by the day: in 2010, the largest container vessel was the Emma Maersk at a carrying capacity of 11,000 Twenty-foot Equivalent Units (TEU), but in April 2020, the HMM Algeciras became the world’s biggest container ship, measuring 400m in length, with a carrying capability of 23,964 TEU.

Large and ultra-large carrier ships run on so-called “bunker fuel”, which is a significant source of air pollution. Shipping currently contributes approximately 2-3% of global carbon emissions, and could represent as much as 10% of global greenhouse gas emissions by 2050. And yet, currently fossil fuels for shipping are enjoying tax incentives compared to alternatives, which is inconsistent with the objective of a lower carbon world.

Who should be responsible for driving reductions in shipping emissions? Critics have argued that the International Maritime Organization (IMO) is ill-equipped to do so. The global nature of the maritime industry makes it hard for accountability to sit with a single organization.

The race for a solution

Ships are big and heavy, and therefore hard to electrify, but pressure is mounting on stakeholders across the value chain for low- or no-carbon solutions. Even if the IMO continues to set non-binding and unambitious targets for carbon, governments and companies are demanding lower carbon solutions from the industry.

In Germany, companies are providing carbon footprint labels for products. In France, a beneficial cargo owner (BCO) can now choose “premium green shipping” and pay more per kilometer to ship the cargo in a more energy efficient way. The top companies in the world see robust environmental, social and governance performance, including a reduction of their carbon footprint, as a necessary condition for business. These companies seek to act ahead of regulation, rather than waiting to be forced into action.

A low-carbon future

There are actions that governments can take now to reduce carbon emissions in shipping. Domestic shipping accounts for at least 18 percent of emissions from the maritime sector, and domestic vessels fall within the control of national governments, rather than the IMO. Electrific and hydrogen fuel cells already exist; the Yara Birkeland is the world’s first electric vessel able to carry 120 TEUs. So while domestic shipping is a relatively small step, it is an important one in paving the way for meaningful change.

While zero-carbon marine fuels are not commercially available today, they are within the grasp of the industry. Liquified Natural Gas (LNG) is, at best, only a short-term solution. While it could reduce carbon emissions, the 20-year warming potential of methane is estimated to be more than 80 times the greenhouse gas effect of CO2, making LNG almost as bad as fossil fuels. New fuels such as Ammonia are promising, but according to McKinsey may reach $1,300-1,500 per ton (compared to $300-500 per ton for fossil fuels).

In order for shipping companies to consider this kind of investment, there needs to be a sound plan to make up for the cost. It could be absorbed by the consumer, with a small increase of less than 1-2 percent to the overall price of the product. A green tax of $150 per CO2 ton, as suggested by Maersk, could be another possible solution. And while environmentally-conscious consumers are likely to agree to this ‘green premium’ idea, it will require data transparency. Big data will therefore play a key role in enabling the future of decarbonisation of shipping.

The power of data

World trade is nearly 32 times greater now than it was in 1950. And while there has been incredible innovation in the global transportation of goods, maritime trade has not yet embarked on the path towards decarbonization. If environmental performance data were readily available, carbon emissions could become a major criteria for trade deals and negotiations.

The first step needs to be measuring every vessel’s emissions on a daily basis. While some energy efficiency measures exist today – such as the IMO’s EEOI and EEDI indices – they don’t capture the full picture. For example, the way a vessel is operated dramatically impacts its fuel consumption and hence its carbon emissions; the same cargo will have a very different carbon footprint, depending on whether it is transported by two smaller vessels or one large vessel.

The last two years have seen some progress, with a flurry of treaties introduced, including the Sea Cargo Charter. But the industry needs to do more. For every single journey, charterers should be able to select the vessels moving their cargo, taking into account their environmental performance. By proactively managing both the cargo leg and the ballast leg (the leg where the vessel is empty and is going to pick up the cargo), and by using technology and big data, charterers can reduce their carbon footprint almost immediately. This can also help improve better commercial terms of the charter party, planning smarter ETA and predicting port congestion - bringing to life the “Virtual Just In Time” that has been in discussions for many years.

And a lower carbon footprint brings increased profitability: for every tonne of carbon saved, businesses will be required to buy one tonne fewer carbon credits to offset the remaining emissions.

With AI, it becomes possible to harness accurate and disaggregated emissions calculations and predictions. This would allow the industry to go beyond historical annual averages, or even emissions by company or individual ship per year. To enable companies to reduce their carbon footprint, we need detailed emissions accounting per voyage by operational activity. This data could be used not only by shipping companies but also by banks, insurers, cargo owners, freight forwarders and everyone down to the end consumer.

Looking ahead

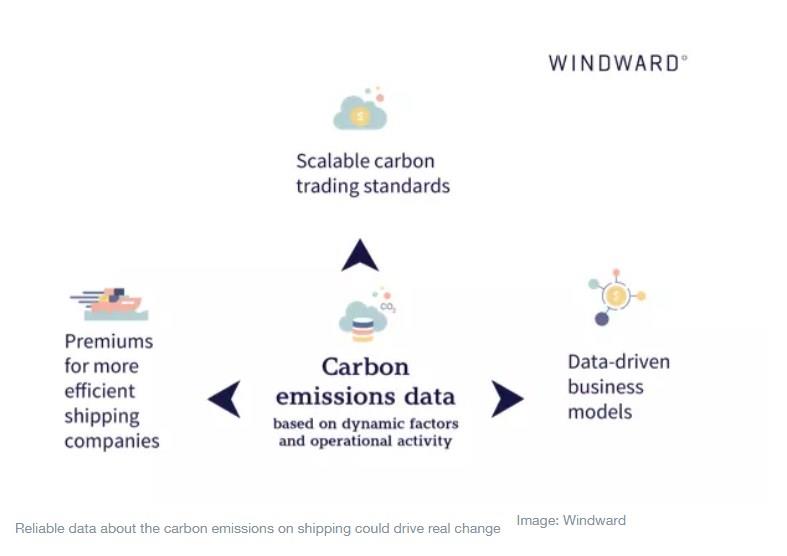

How will this data impact the industry? We can expect new and data-driven business models, premiums for more efficient shipping companies, and globally scalable carbon trading standards. These will create a strong economic incentive for companies to be carbon efficient, without setting the industry back.

From a consumer perspective, being able to access reliable data about the carbon emissions on shipping could drive real change: if each one of us knew the carbon impact of everything we bought, from our clothes, to our car, to the food we eat, we could use that to inform our choices. Stock values, press, brand reputation, and bottom-line revenues will all be susceptible to this change.

It’s time for shipping to step out of the shadows, to be forthright and act boldly, taking the initiative on carbon before the industry is forced to take action. Waiting for regulation to emerge from an agency and effectively drive change is not the right answer. Real cooperation between shippers, regulators, financiers and technology companies to drive sustainable impact is the only way to both protect our environment and the long-term interests of the industry.

*Co-Founder and Chief Executive Officer, Windward and Chairman, BeyondNetZero, and Chairman, Windward

**first published in: www.weforum.org

By: N. Peter Kramer

By: N. Peter Kramer