by Charlotta Groth*

The green lining of the COVID-19 crisis is a projected 8% drop in global CO2 emissions in 2020. Unfortunately, this barely takes emissions back to where they were a decade ago, and the true eyeopener is that the 8% fall only matches the pace of decline needed every year until 2050 to limit the rise in global temperatures to 1.5°C (which would be in line with the Paris Agreement).

The 8% decline has moreover come alongside the deepest recession since the Great Depression of the 1930s. This unprecedented experience shows that the only way to realistically tackle climate change is to decouple CO2 emissions from economic activity. While possible, this requires very large and transformative investments – in new technology, in the electricity grid, in energy storage capacity, and in large-scale energy efficiency measures. Here, the COVID-19 crisis ought to act as a trigger, as economic support measures could be used to launch green investment projects and reposition the global economy for a greener future.

The pandemic has prompted an unprecedented wave of stimulus. Fiscal support announced since January amounts to $5 trillion, and central banks have injected more than $6 trillion into financial markets. While profound, these emergency steps have certainly not been green, and there are fears that the COVID-19 recovery will be a missed opportunity to shift the trajectory on climate change. This is what happened after the financial crisis of 2007-2008, when the kick-starting of growth eventually triggered a commodity price boom, a surge in fossil fuel investment and a steep increase in CO2 emissions that will be locked into the atmosphere for thousands of years.

While not green, the stimulus has nonetheless raised global debt – from an already elevated level – and will have a lasting impact on public finances, at what is an unfortunate point in time. To reposition the global economy and energy systems in line with a 1.5°C scenario, an estimated investment of more than $90 trillion will be required over the next 15 years. Not all of this can be publicly financed, but governments will have to lead the way and be part of the solution. With limited fiscal space, resources must be used wisely, which is yet another reason why support measures to contain the COVID-19 crisis should target climate change.

There are still hopes for the next round of stimulus. The EU’s recovery plan, which amounts to close to €1.8 trillion ($2.1 trillion), is set up to support the recovery and kick off a multi-decade green investment wave. One third of funds have been earmarked for climate action, making it the greenest fiscal effort so far. The idea is that this will help to close the green investment gap – necessary to meet the EU’s 2050 net-zero emission target – by also pulling in private investment initiatives. It still needs to be agreed by the European and national parliaments, but this is an important step forward and raises prospects for generating a more sustainable recovery. Other countries need do more to catch up with the EU in this regard.

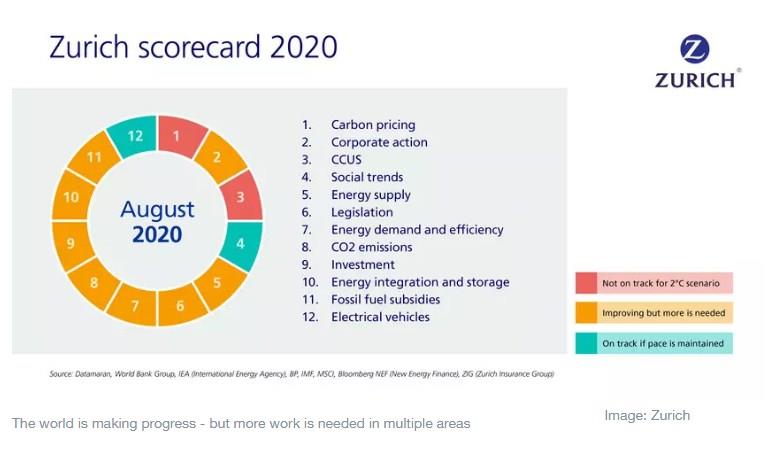

Once again, our scorecard on climate change (see above) sends out a clear message - changes in behaviours and technology are insufficient for the global economy to transition towards a 2°C compliant world. Moreover, the global pandemic is, by itself, unlikely to shift the trajectory on climate change. While the fall in CO2 emissions is welcome, a path towards sustainable reductions is – as yet – missing.

*Global Macroeconomist, Managing Director, Zurich Insurance Group

**first published in: www.weforum.org

By: N. Peter Kramer

By: N. Peter Kramer